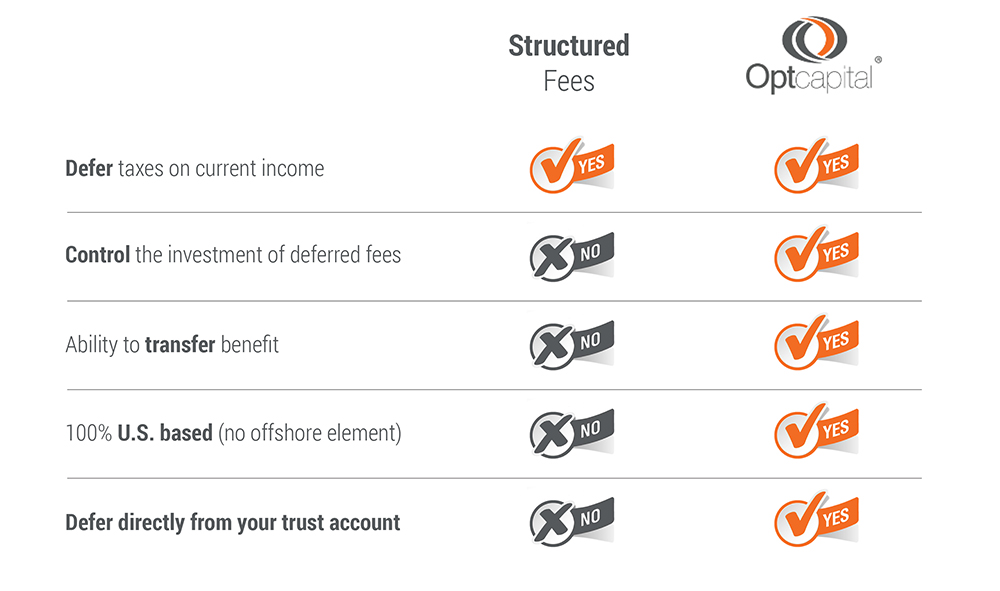

Optcapital’s deferral program is designed specifically and exclusively for plaintiffs’ attorneys, and offers a demonstrably better alternative to structured fees.

Program Highlights

- Invest an unlimited amount on a pre-tax and tax-deferred basis

- Deferred fees are invested with your Financial Advisor.

- Highest level tax opinion for 15+ years.

- Can defer directly from your IOLTA account, without involvement of defense counsel.

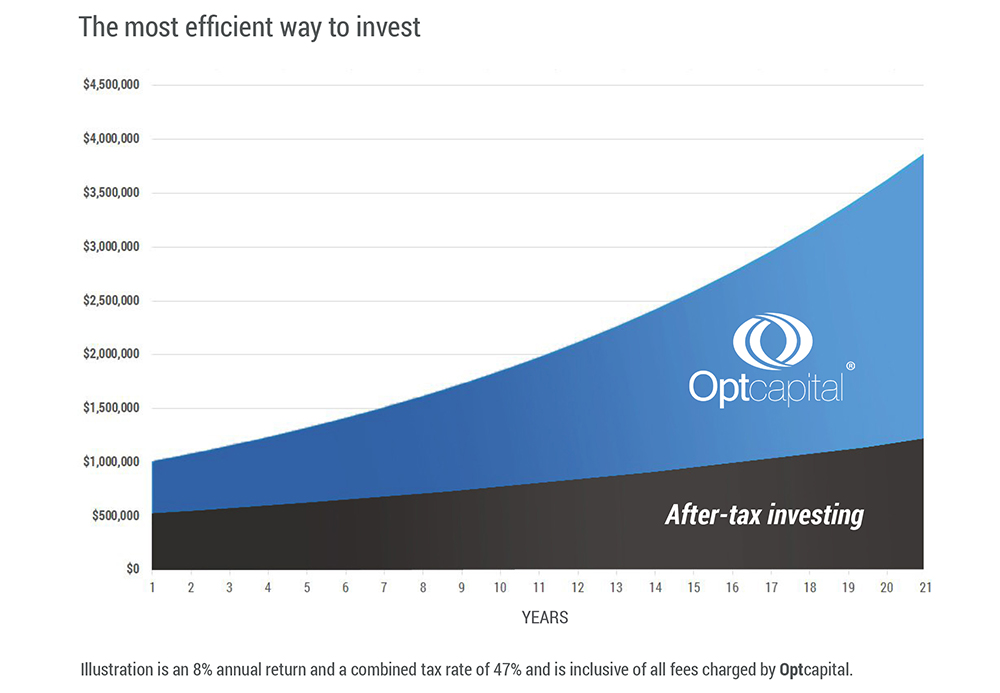

Tax deferred investing has two advantages:

- You invest fees on a pre-tax basis. If you earn a $1 million fee, you invest the full $1 million rather than the after-tax amount (assume $600,000), providing a greater opportunity for appreciation.

- You do not pay taxes on gains so long as the funds are in the account. If your $1 million deferral increases by 10%, you have $1.1 million. On an after-tax basis, if your $600,000 grew by 10%, you would pay taxes on the $60,000 gain, leaving you with roughly $640,000.

The chart below illustrates the power of investing on a pre-tax and a tax-deferred basis.